This is not going to make me very popular, but every way I look at SpaceX stock shows that it is overvalued. By a lot!

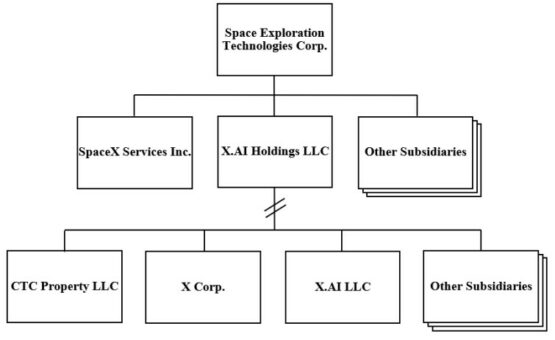

For those living under a rock, SpaceX is a smooshing together of two Elon Musk companies: SpaceX/Starlink and his Twitter acquisition, renamed X, which has spun up yet another LLM called Grok (to rename the entire thing to X.AI Holdings).

SpaceX corporate structure

Source: SpaceX IPO documents

In classic Musk-style, he has used his successful company (namely, Tesla and/or SpaceX) to hoover up his loss-making disaster (namely, SolarCity and/or X.AI Holdings).

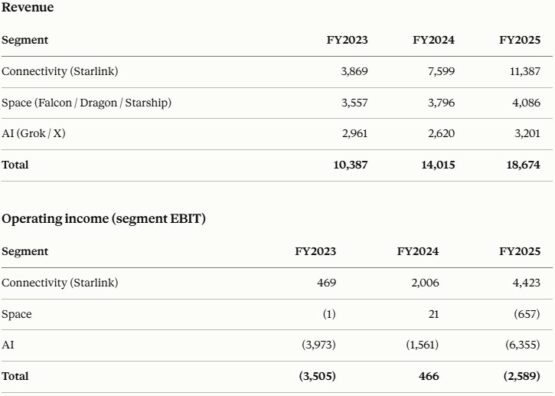

How loss-making?

Well, in FY25, “Connectivity” (i.e., Starlink) is SpaceX’s profit engine, generating $4.4 billion in operating profit on $11.4 billion in revenue. SpaceX’s “Space” segment turned $4 billion revenue into a $0.5 billion loss.

While “AI” (i.e. X.AI Holdings) generated $3.2 billion in revenue and reported a gigantic $6.3 billion operating loss.

ADVERTISEMENT

CONTINUE READING BELOW

And, here’s the trick, you cannot invest in just Space and Connectivity alone. If you invest in SpaceX, then you also have to invest in (in other words, subsidise) the deeply questionable X.AI cash-burn.

SpaceX’s reporting segments

Source: Summarised SpaceX IPO documents

But surely this is just a snapshot in time and, much like Tesla, the group is investing now (that is, making a loss) so that in the future it can earn super profits?

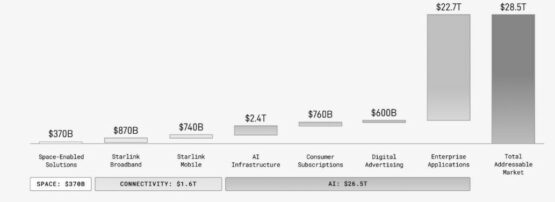

Well, this is where SpaceX’s own disclosure is interesting, as it reveals what it believes its “Total Addressable Market” (or “TAM”) is per segment.

(Think about TAM as the total market size, such that if a company addressed 100% of TAM, the company’s revenue would equal the market size, as 100% of sales here would be the company’s.)

SpaceX’s segmental total addressable market (TAM – $bn)

Source: SpaceX IPO documents

This is going to irritate the bulls, but I am just plain going to ignore X.AI’s TAM as a dystopian future whereby all humans are replaced by AI (which also means that all consumers are broke, so who exactly is buying the outputs of this system of horrors?). Rather, I will focus only on Space and Connectivity’s TAM.

ADVERTISEMENT:

CONTINUE READING BELOW

Collectively, Space and Starlink have a TAM (as disclosed by SpaceX, so this is the optimistic version of it!) totalling $1,980 billion.

Well, $1.9 trillion is close to the (at the time of writing this) $2.5 trillion that SpaceX’s market is trading at, right? Maybe add a little option for X.AI, and we have a justifiable valuation?

Nope, not even close.

TAM is sales, not profits. Even if you addressed 100% of a potential market, you still have costs to consider. And, if SpaceX’s IPO documents and most optimistic forecasts are anything to go by, SpaceX has a lot of costs.

Maybe forecasts show some great upside?

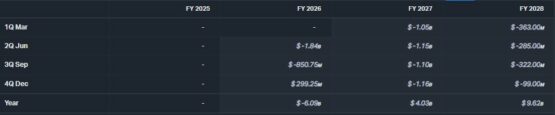

Well, also nope, as despite analyst consensus forecasting basically a tripling of sales, the group only grinds out losses for incoming periods … Maybe one day there will be material profits for shareholders, but you have to be in this one for the long haul to get them.

SpaceX’s broker consensus earnings before interest & tax (Ebit)

Source: Koyfin (18/06/2026)

ADVERTISEMENT:

CONTINUE READING BELOW

Perhaps another way to phrase this is that SpaceX is currently trading on an enterprise value-to-sales (EV/Sales) of 131 times.

If SpaceX’s revenue carries on at current levels, the company literally never incurs a single expense (in other words, revenue equals profits) nor pays taxes, and pays out all of this unrealistic profit to shareholders, it will still take a century and 31 years to get just your capital back (with zero return).

A lot can be said for Musk, his followers, the hype that follows and how SpaceX has gamed the passive markets via indices (combined with a small free float) to force this listing, share price and valuation.

Read:

Humans can get caught up in all this as well as dreams of space (what is the “TAM” of Mars? What multiple do I put on “taking the light of consciousness to the stars”?), which is why I ran a token-heavy Claude Discounted Free Cash Flow Model on SpaceX based on its own IPO documents – none of the market’s optimism here nor my own bias allowed.

Claude’s cold-hearted conclusion is that a 10-year DCF values SpaceX’s equity at roughly $3.49 to $10.59 per share. This is a small fraction of the $135 offer price, and even less of the current c.$200 per share market price.

Because the index investors are being forced to buy the company with extreme urgency (it is large in indices) and its free float (what the index investors can buy) is small, SpaceX’s share price could well go higher for the time being … But for how long can its rockets defy the gravity of its valuation?

* Keith McLachlan is CEO of Element Investment Managers.

#SpaceX #overvalued #Moneyweb