Hedge fund manager Lee Robinson notched a 900% gain during the global financial crisis by turning a $20 million position into $200 million with timely bets against the US subprime mortgage sector.

Today, he sees a new opportunity as risks bubble up around private credit. But instead of betting directly against the sector, he’s focused on potential second-order effects and is shorting some of the $1.8 trillion market’s biggest backers: insurers.

Robinson is ramping up bearish wagers on firms from Lincoln National Corp to MetLife and even Berkshire Hathaway Inc. through the use of credit default swaps, derivative contracts designed to protect investors against a default. His firm, Altana, is launching a new fund, into which it is also investing its own capital, to protect against what he sees as an inevitable downturn in private credit, a cooling-off in AI hype, and the impact of declining liquidity on corporate valuations.

He says there are parallels between the general calm that prevailed in the subprime mortgage market before the blowup of Lehman Brothers Holdings Inc. and markets today, where corporate yield premiums remain at historically low levels. That investor confidence — or overconfidence, as Robinson sees it — persists even as concerns simmer about private credit’s exposure to software borrowers under threat from artificial intelligence, and as warning signs flash from a couple of corporate blowups.

“In August 2008, we were pulling our hair out, wondering how on earth volatility is at this low level,” Robinson, founder and chief investment officer for London-based Altana Wealth, said. “It feels a little like that now.”

It’s not that insurers face an existential threat from their exposure. Robinson’s argument is more nuanced: He believes markets aren’t adequately pricing in the added risks of writedowns from an untested corner of debt that has shown itself prone to trouble spots. Holdings of private credit are rising in the industry, particularly among life insurers, and while the debt is still a relatively small part of many established firms’ investments, it does present risks, he said. Another attraction of the trade is that it isn’t easy to short private credit directly.

Lincoln National didn’t respond to a request for comment while a spokesperson for Berkshire Hathaway declined to comment. A spokesperson for MetLife pointed to recent comments by Chief Financial Officer John McCallion that around 95% of its private debt portfolio is investment grade, “well diversified and built to perform across market cycles.”

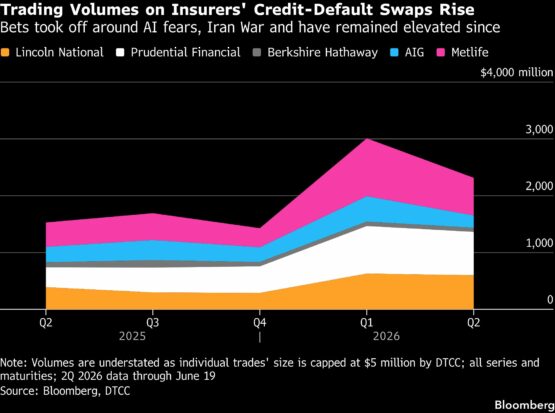

Increased activity

Robinson’s gambit is starting to spread. Other hedge funds are targeting insurers’ CDS, and Wall Street desks including JPMorgan Chase & Co. and Goldman Sachs Group Inc. are also getting involved, responding to client requests with products that provide protection against risks swirling around the industry, people familiar with the matter told Bloomberg.

ADVERTISEMENT

CONTINUE READING BELOW

Representatives for JPMorgan and Goldman declined to comment.

Net notional bets on US insurers’ CDS have risen to $5.5 billion by May 22 from less than $4.9 billion at the end of last year, based on data by the Depository Trust and Clearing Corp. Trading volumes in those contracts has also seen an increase, and the price to buy default protection has started to rise — though only marginally compared with the potential risks involved, leaving room for further gains in the event of a true meltdown.

Insurers’ exposure to the private credit industry has grown significantly over the last decade as asset managers sought yield and diversification, particularly during the easy-money era when traditional assets were yielding close to zero. A Moody’s Ratings analysis of US life insurers showed that a fifth of the sector’s $4 trillion of fixed-income holdings were allocated to illiquid assets, mostly private credit, at the end of 2025, up from 18% the year before.

The move to private credit has been particularly pronounced among the life insurers owned by asset management giants with private equity arms such as KKR & Co. and Apollo Global Management Inc., according to researchers at the Federal Reserve Bank of Chicago, though there is no suggestion that Robinson and others have been targeting those firms in particular. The shift has been primarily into investment grade-rated private debt.

“Insurers have become intertwined with the broader private credit ecosystem,” authors Ralf Meisenzahl, Jackson Overpeck and Andy Polacek wrote in a working paper last revised in late April.

Representatives for Apollo and KKR declined to comment.

Some insurers have been vocal about their activity. Last year, Lincoln Financial launched a fund with Bain Capital to “provide individual investors access to private credit.” MetLife said it held about $85 billion of what it deemed “high-quality” private fixed income as of March 31.

ADVERTISEMENT:

CONTINUE READING BELOW

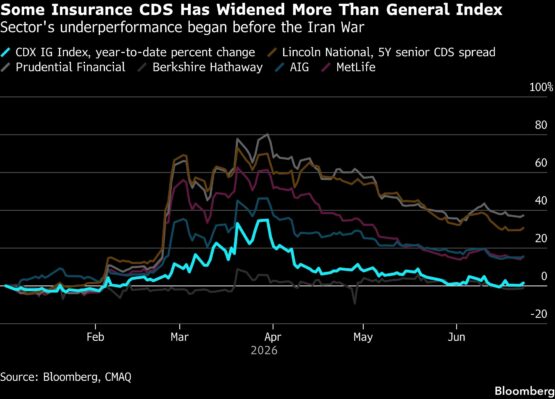

Already, the cost of protection against defaults by US insurance heavyweights including American International Group Inc. has started to rise, exceeding that of a broad gauge of North American high-grade risk this year, based on data compiled by Bloomberg. That’s seen in widening CDS spreads.

It’s a similar picture with European giants Allianz SE, Generali, Aviva Plc and Axa SA compared to the region’s own high-grade credit-default swap index. So much so, that it has caught the attention of the European Central Bank, which sent out a warning about potential losses for insurers.

An Allianz spokesperson cited an earnings presentation and analyst call in which executives at the firm said they are comfortable with the private debt exposure and that they have a “very high quality, diversified portfolio.” Aviva declined to comment, while Axa and Generali didn’t respond to a request for comment.

Even after some recent widening, CDS spreads in these companies are still quite tight, limiting potential downside for investors. Lincoln National, for example, was last quoted at 142 basis points. That reflects some recent widening, but is miles away from where a truly troubled company would trade, and on par with many of the world’s largest companies.

“There’s going to be more pain for private and institutional investors going forward and insurance companies will probably have to partially write down their investments,” said Mark Lieb, chief executive officer at Spectrum Asset Management, who has been active in preferred securities since the 1970s.

Connecticut-based Spectrum specializes in junior securities that companies, including insurers, sell to pad their financial health, often at the behest of regulators.

ADVERTISEMENT:

CONTINUE READING BELOW

“The insurance side, we monitor that closely. Some insurance companies have gotten a little more aggressive with their private placements,” Lieb said. “We’ve made some internal changes on what we like and don’t like in some of the names, so you have to be a little bit more vigilant of that part of their portfolio.”

Distressed debt wagers

Robinson for his part is spreading his bets within his new fund, investing in single-stock equity options in addition to insurance CDS. Robinson, who previously worked for hedge fund billionaire Paul Tudor Jones, has a track record with opportunistic and distressed debt wagers.

Back during the global financial crisis, Robinson allocated a small portion of his funds into a bet against subprime mortgages, and by doing so he generated an outsized profit. This successful bet helped propel his two Trafalgar funds to gains of 5% and 26% respectively for the year 2008, compared with an average decline of 18.3% for the wider hedge fund industry.

Elsewhere, Robinson launched a digital currency fund in 2014 that has gained significantly since inception, and made winning wagers on Lebanese sovereign debt and Fannie Mae junior preferred securities. His Credit Opportunities fund is up 47.5% year to date, and 416% since inception in 2020. Meanwhile, one big bet he made related to Credit Suisse remains unresolved; his funds own claims on Additional Tier 1 bonds wiped out with the bank’s collapse and takeover by Swiss peer UBS. A lengthy legal battle is underway.

Regulators paved the way for private credit to balloon in size after the global financial crisis, imposing onerous requirements for traditional lenders that prompted banks to retreat from some of the riskier, more capital-intensive parts of their business. This created a gap that private credit firms pounced on. Insurers needing to match assets with liabilities were ready buyers of the assets.

While the reasons for the shift may be understandable, it poses complexity and concentration risks, Moody’s Ratings analysts led by Manoj Jethani said in a note this month. “Risks are emerging — particularly in middle-market direct lending — driven by weaker credit quality and rising borrower stress,” they said.

All it would take now, Robinson says, is one stressed insurer — “any single blow-up” — to cause ripples throughout the industry.

© 2026 Bloomberg

#Investor #scored #win #crisis #big #short #bet