For anyone trying to work out where US interest rates go from here – and what that means for their portfolio – Kevin Warsh’s first press conference as Federal Reserve Chair was the event to watch.

Markets came away convinced that the US will hike interest rates before year-end, reading Warsh’s debut as a hawkish turning point.

Our interpretation is more nuanced.

Read:

US Fed holds rates steady

Copper falls after Fed chairman Warsh positions as inflation hawk

Gold extends gain after Warsh remarks ease rate-hike prospects

At a press conference the chair’s job is usually to reflect the consensus of the Fed’s rate-setting committee, the FOMC [Federal Open Market Committee], rather than to push a personal view. That matters here, because Warsh’s debut came under unusually close scrutiny.

He was appointed by President Trump after the administration spent much of the year testing the limits of the Fed’s independence, and every word was parsed for signs of political influence. In that setting, Warsh largely worked within the framework he inherited, while signalling that it is likely to evolve over time rather than be torn up overnight.

Even so, the updated ‘dot plot’ – the chart on which each official marks where they expect rates to go – still showed nine of 18 participants pencilling in a hike before year-end.

We think markets are placing too much weight on that signal.

While nine of the 18 participants projected a hike this year, only 12 of them actually vote on policy. Based on our reading of recent

speeches and public communications, we think it more likely than not that at least eight of those 12 voting members have yet to signal support for a hike this year.

While encouraging his colleagues to submit their dots, Warsh notably declined to submit a dot of his own – a subtle but deliberate move.

Read:

Fed minutes show more officials warned of rate-hike scenario

Warsh’s first FOMC: What it signals for the road ahead

Rather than imposing a new framework on the committee straight away, he set a new direction from day one while keeping his colleagues inside the process and giving them ownership of how it evolves. In doing so he quietly reduced the signalling weight of the dot plot and, more broadly, the authority of the inherited framework and his colleagues’ projections; without alienating the room.

ADVERTISEMENT

CONTINUE READING BELOW

He paired this with a pointed critique of the previous regime, and of the framework itself, noting that it had failed to deliver price stability over the past five years.

Yet he was unequivocal that this committee willa chieve price stability – a goal the whole committee can unite behind – even as he begins to reshape what getting there actually requires. Crucially, he left the ‘how’ deliberately unspecified.

The message was clear: Warsh is steering the Fed onto a new path which he believes will prove more effective at delivering price stability – and he is doing it through participation and consensus-building rather than a clean break from the existing framework.

There is a task force for that

The announcement of five task forces is the first concrete step in embedding that new direction. Their structure clearly reflects Warsh’s known views, even as he stressed that he would not prejudge the outcomes and framed the exercise as an open-ended, first-principles review.

The most consequential, we think, is the one examining the inflation framework – particularly if it validates Warsh’s view, which we broadly share, that liquidity (the sheer quantity of money available to be spent or invested) has been a meaningful driver of both inflation and asset prices in recent years, contributing to the breakdown of several previously stable economic relationships.

If that link holds, it strengthens the case for the balance-sheet task force, which will examine how money created through the Fed’s balance sheet feeds into financial conditions – shaping risk appetite and lending and, when liquidity is excessive, occasionally fuelling bouts of market froth.

Read:

Fed’s Warsh rocks bond market in debut, sparks surge in rate-hike bets

Fed chair contender is now in favour of cutting rates, just as Trump wants

The remaining three task forces cover Fed communications, data and economic measurement, and productivity and employment – reinforcing Warsh’s preference for a genuinely data-dependent framework that leans more on the quality of the data and less on forward guidance, the practice of steering markets by signalling future moves in advance.

Taken together, the five point to an incremental but meaningful broadening of how the Fed operates: away from a purely rate-centric view of policy and towards a more explicit recognition of liquidity and balance-sheet channels as well.

Warsh reinforced this when asked whether policy is still restrictive, noting that its effects are uneven – restrictive in parts of the real economy, particularly housing, but far less so in financial markets, where liquidity remains abundant.

Liquidity looking for an outlet

ADVERTISEMENT:

CONTINUE READING BELOW

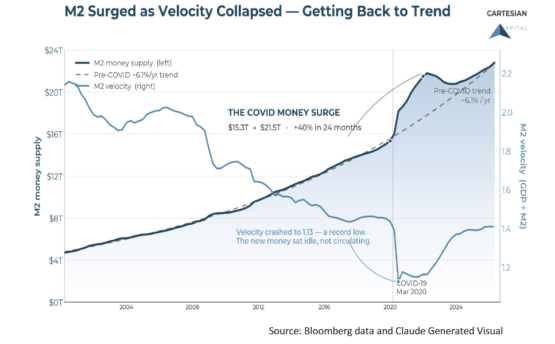

The case for giving liquidity a bigger role in the new framework starts with the money created during the pandemic. Using M2 – a broad measure of the readily spendable money in the economy, spanning cash and deposits – as our proxy, the money stock swelled from roughly $15.4 trillion at the start of 2020 to around $22.8 trillion today.

That steep, near-parabolic 48% jump durably reset the economy’s liquidity base to a structurally higher level.

But the level alone understates what happened. In our view it was the pace of the expansion, as much as its size, that did the lasting damage.

Money was created far faster than the real economy could absorb or productively deploy it, and that speed broke relationships that policymakers and investors had long relied on – above all the stable link between money growth, economic activity, and prices.

When the normal channels are overwhelmed, money is not destroyed or lost; it simply finds another outlet. The extraordinary expansion in M2 clearly contributed to inflation in recent years, but we would argue that a meaningful share of that liquidity bypassed the real economy and was absorbed into asset prices instead.

Read: Warsh may need five years to really shrink the central bank’s balance sheet

The velocity of M2 (how quickly each dollar changes hands as it circulates through the economy) illustrates the distortion. It collapsed to a record low during the pandemic, as the largest expansion in the money supply in modern history outran the economy’s ability to use it.

It is not conclusive, but the fact that velocity remains below its pre-pandemic norm, even now that money-supply growth has returned to trend, is consistent with part of that liquidity continuing to circulate primarily through financial markets rather than the real economy.

Encouragingly, M2 growth has largely reverted to its long-run trend, and the money stock is no longer materially above its pre-pandemic trajectory. Still, we think the legacy of the rapid pace of the prior expansion has not fully unwound.

This is not to suggest that liquidity should replace the policy rate as the primary policy tool. Rather, even with policy rates still restrictive on our estimation, liquidity dynamics continue to matter for asset prices and inflation.

A framework that prices money but underweights how much of it there is, and how fast it arrived, is in our view missing a key part of the transmission mechanism – the chain through which policy actually reaches the economy and markets.

ADVERTISEMENT:

CONTINUE READING BELOW

Where this leaves investors

The eternal question: what does this mean for portfolios into year-end?

Read: The Fed’s bold move: What it means for investors

Start with the lay of the land

The market has taken Warsh’s debut as hawkish and priced a hike before year-end accordingly, but we would be wary of leaning too heavily into that view. Our sense is that the bar for a hike this year remains high, leaving scope for some of that hawkish repricing to unwind.

The more interesting possibility, though, is that the hawkishness was the point. By sounding tough in his first meeting, Warsh banks anti-inflation credibility upfront and, having earned it, can gradually reorient policy in the consensus-building manner he outlined, without unsettling markets.

If that is the play, he gets what he wants, a Fed steered onto a new path without sacrificing credibility, entirely in keeping with the operator who managed the dot plot and introduced the Fed’s new task forces.

Either way, the more durable signal for investors sits beneath the policy rate. The signal to watch, in other words, is shifting from the level of interest rates to the quantity of money behind them; and investors still watching only the rate may find they are reading yesterday’s map.

Kyle Coertze is an investment analyst at Cartesian Capital.

#Warshs #Fed #liquidity #dot #plot